Wondering if GUARDD is right for you? We put together this section so that we could answer some of the top questions we get.

1. Why would I want to make my private business and financial information public?

2. What is GUARDD?

3. What is RIVIO?

4. Why is GUARDD using RIVIO?

5. What does RIVIO stand for?

6. Who is RIVIO for?

7. How does RIVIO validate CPA firm users?

8. Who is CPA.com?

9. Examples of companies who would benefit from GUARDD

10. In which states does the manual exemption apply?

11. What do I do in the other states?

12. What is 2-11 reporting and how does it relate to what GUARDD does?

13. Do I have to be truthful on my GUARDD filing?

1. Why would I want to make my private business and financial information public?

Companies that choose to use GUARDD do so for multiple reasons. First, they believe that fulsome and continual disclosure about their business and financial information is in the best interest of their shareholders. Second, they understand that there are federal and state laws that govern the continual disclosure of business and financial information and while some of them may not pertain to them, others (like Blue Sky laws) do and they aim to be in compliance with them. Third, companies that wish to have their securities available for secondary trading need to have a system in place to make disclosures available to purchasers of these securities as well as material updates.

2. What is GUARDD?

GUARDD is a reporting tool that is used by private companies that wish to publish their business and financial information. Not all companies need GUARDD but if you have a reporting requirement that requires you to keep your investors up to date about what is happening in your business, then GUARDD may be right for you. It is an online tool that allows you to enter, update and publish your business and financial information on a quarterly, semi-annual or annual basis. If you have audited financials, GUARDD is integrated with RIVIO such that people that have access to your GUARDD report can also click through to see your audit report. It turns the burden of “how do I do semi-annual reporting to my investors” into a stress-free fill in the form process that creates an easy to understand report.

3. What is RIVIO?

RIVIO is an online financial document clearinghouse that enables private businesses to exchange key financial information with their investors and lenders as well as retrieve information from their CPA firm, ensuring data is submitted from an authenticated source. Developed by CPA.com, a subsidiary of the American Institute of CPAs, in partnership with Confirmation, the secure, digital platform verifies that CPA firms leveraging the clearinghouse are appropriately following the stringent professional requirements to upload attested financial information.

4. Why is GUARDD using RIVIO?

The connectivity with GUARDD enables efficient, secure access to view audit reports that have been protected from alteration and provided by a licensed CPA firm.

5. What does RIVIO stand for?

RIVIO Stands for Repository for Independently Validated Input and Outputs

6. Who is RIVIO for?

RIVIO was designed for Private Businesses, their CPA firms, and their key Third Parties (banks/lenders, board of directors/advisors, regulators, investors/shareholders, etc.); any entity to which a private company would exchange financial statements or reports prepared by their licensed CPA firm

7. How does RIVIO validate CPA firms users?

The clearinghouse provides CPA firm validation by confirming that the firm meets the following criteria:

-

Licensed with the appropriate State Board of Accountancy

Current in their relevant peer-review commitments

8. Who is CPA.com?

CPA.com brings innovative solutions to the accounting profession, either in partnership with leading providers or directly through its own development. The company has established itself as a thought leader on emerging technologies and as the trusted business advisor to practitioners in the United States, with a growing global focus.

A subsidiary of the American Institute of CPAs, the company is also part of the Association of International Certified Professional Accountants, the world’s most influential organization representing the profession. For more information, visit CPA.com.

9. Examples of companies who would benefit from GUARDD

a. Any company that wishes to have a standard reporting tool to summarize their business and financial information and make this available to investors.

b. Any company with a reporting requirement that requires you to keep your investors up to date about what is happening.

c. Any company that is seeking Blue Sky exemptions and must provide regular updates to investors about a company’s well-being.

d. Any company that raised money under Regulation A+ and wishes to allow their securities to be sold on secondary exchanges.

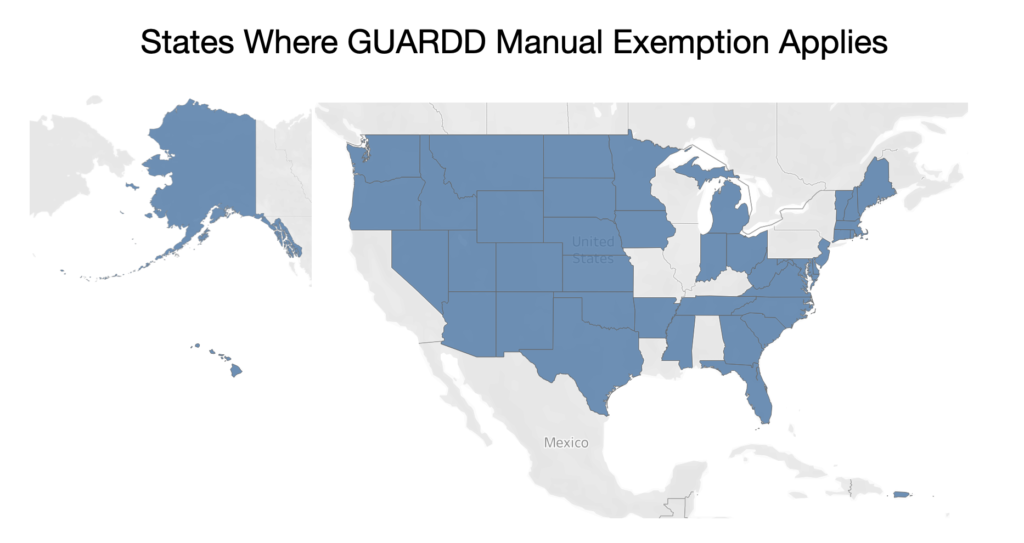

10. In which states does the manual exemption apply?

The manual exemption requires that your ongoing disclosures be published in a nationally recognized securities manual. You GUARDD report gives you coverage in the following states:

11. What do I do in the other states?

These are the following states that do not allow for manual exemption. If you are not making your securities available to residents in these states you may not have to register them. If you are, in most cases, you would need to register your securities. The states are: Alabama, California, Illinois, Kentucky, Louisiana, New York, Missouri, Pennsylvania, Virginia

12.What is 15c2-11 reporting and how does it relate to what GUARDD does?

There are public companies and there are private companies. Public companies list their shares on exchanges (like NYSE, OTC Markets, NASDAQ, etc) and must keep investors informed about a company’s well-being via quarterly and annual filings (sometimes known as 10-k’s and 10-q’s). The reporting requirements for public companies fall under Rules 15c2-11 of the Exchange Act.

Private companies that wish to allow their shares to be traded (and not on exchanges like NYSE, OTC Markets, NASDAQ, etc) must comply with State Blue Sky Laws. These are individual state laws regulating the sale of securities, intended to protect the public from fraud. Not all States have Blue Sky laws and of those that do, the law usually differs. The general gist is that if a company wishes to allow their securities to be sold to investors in their state the company must either register and file with the state or be exempt from filing. Either registration or exemption usually includes continual update and reporting on the company’s business and financial operations. GUARDD helps those private companies publish their business and financial information so that they can be exempt from or in compliance with State Blue Sky Laws.

GUARDD is very much like the reporting requirements under Rule 15c2-11. Rule 15c2-11 requires that the company have current public information available before the market maker can quote the security. The information required in the Form 211 satisfies the current public information requirement of Rule 15c2-11.

Form 211 requires, among other things, the following disclosures:

- Whether any officer or director of the issuer had any regulatory action taken against him/her by the SEC, NASDAQ, NYSE or other securities-related regulatory agency and whether any officer or director of the issuer has been convicted of any felony charges within the prior 5 years;

- Detailed description of the issuer’s business, products/services offered, assets and sources of revenue;

- Description of the company’s facilities including the location, square footage and whether owned or leased;

- Identification of officers, directors and holders of more than 5% of the company’s securities;

- Certificate of Incorporation and bylaws including any amendments;

- Current transfer agent generated shareholder list, indicating name and address of each shareholder, the number of shares owned, date of share ownership, and whether the shares are restricted, control, or free trading;

- Description of the company’s free-trading shareholder base, including a description of exemptions from registration under the Securities Act;

- Agreements creating restrictions, liens or encumbrances on, or relating to, the transfer or voting of shares;

- Agreements evidencing stock rights, warrants or options;

- All stock purchase or asset purchase agreements for last five (5) years;

- Disclosure of whether the company has entered into any discussions or negotiations concerning a potential merger or acquisition candidate;

- Merger and/or consolidation agreements;

- Partnership and/or joint venture agreements;

- Unaudited financial statements for the last 2 fiscal years and interim periods;

- Details of all private offerings including who solicited investors, how they were known to the solicitor, and how many individuals were solicited, and whom did not purchase;

- One full copy of the subscription agreement executed by each investor and copies of all checks from the subscribers or other proof of payment;

- Copies of Form D filed with the SEC;

- Description of all relationships among and between every shareholder and the issuer, its officers and directors, and other shareholders;

- A statement indicating whether any person or entity has control, written or otherwise, of the sale, transfer, disposition, voting or any other aspect of the shares listed on the shareholders list other than the shareholder;

- A detailed business plan, which includes a detailed chronological account of each and every step the issuer has taken in furtherance of its stated objective since inception;

- A description of the steps the Company plans to take during the next year in furtherance of its business plan, including the activities in which the Company plans to engage, the names of the persons who will conduct these activities, and the expected dates of these activities;

- A description of any future financing plan;

- Any material agreements or letters of intent entered into by the Company;

- Schedule of all material patents, trademarks, trade names, service marks, and copyrights; and

- Legal opinion from company‘s securities lawyer as to tradability of the free trading shares.

13. Do I have to be truthful on my GUARDD filing?

Your GUARDD filing will potentially be seen by current investors, prospective investors and regulators. As such it is mandatory that you complete as much of the report as possible and with 100% accuracy in mind. The information that you enter in this report is not verified by GUARDD. As such, it is your responsibility to be truthful in what you represent. There is an officer attestation required at the end of the report that is similar to the type of attestation a CEO / CFO is required to make during the course of an audit. Access to the GUARDD manual is shared with state and other regulatory authorities and with the public, so any false or misleading statement or material omission made in connection with a securities offering would violate the Securities Act and/or state laws. You should both complete and have your GUARDD report reviewed by your counsel